Bankruptcy can make sense depending on your debt load, financial commitments, and whether you have tried other debt relief options.

Filing for bankruptcy does not mean you are a failure; in fact, it might even help you start over financially.

Bankruptcy prevents wage garnishments, litigation, and collection calls. Contrary to popular belief, bankruptcy can actually improve your credit ratings by eliminating certain types of debt.

Bankruptcy, according to credit bureaus and scoring specialists, is the worst thing you can do to your credit ratings. Nothing can lower your credit scores as quickly and significantly as filing for bankruptcy, including charge-offs, collections, repossessions, and foreclosures.

That is not the whole tale, though. Many people battle their debt for so long that by the time they declare bankruptcy, their credit has already suffered. And when they do, their scores usually increase rather than decrease. Scores increase further if the debt is discharged, referred to as a “discharge” in bankruptcy court.

Potential benefits of filing for bankruptcy

The potential for a new financial beginning is one of the main benefits of declaring bankruptcy. Although filing for bankruptcy is not a quick remedy, having your unsecured debts discharged (as in Chapter 7 bankruptcy) may provide you with a fresh start that enables you to make improvements to your financial situation and habits. Other possible advantages of declaring bankruptcy include:

An end to ongoing debt collection: Those who declare bankruptcy take advantage of its “automatic stay,” which stops practically all forms of collection, including wage garnishment and litigation. The lawsuits and garnishment stop once the underlying debt is paid off.

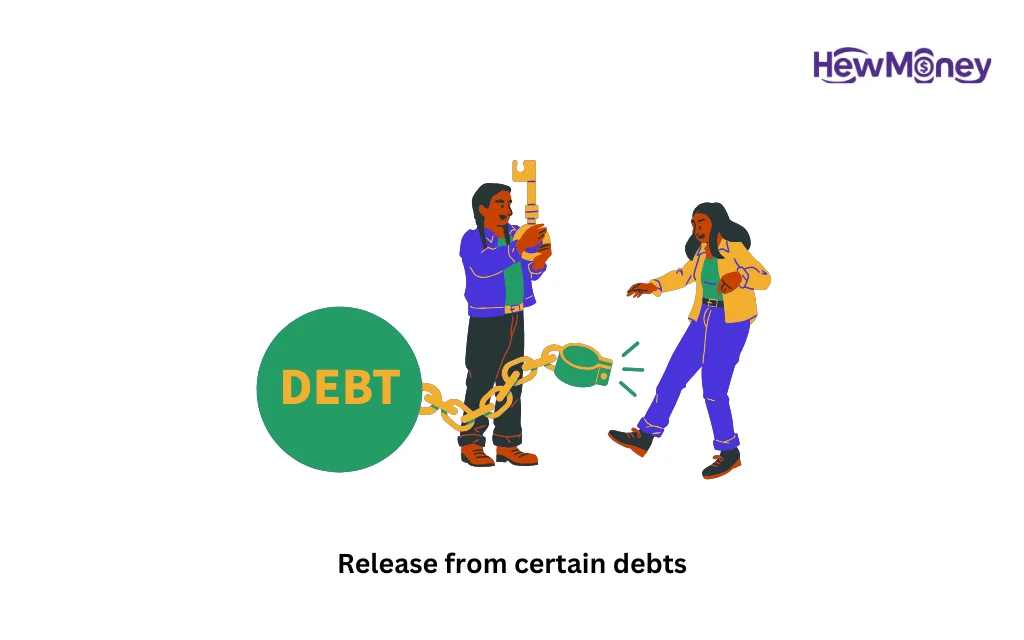

Release from certain debts: Chapter 7 bankruptcy eliminates a variety of debts, such as:

- debt from credit cards.

- medical expenses.

- individual loans.

- civil rulings (apart from fraud).

- Rent that is past due.

- unpaid utility bills.

- company debts.

- a few previous tax obligations.

Child support and current tax obligation are among the debts that cannot be discharged in bankruptcy. Although it is uncommon, student loan debt can be. Erasing other obligations, however, may allow you to pay back what is left over if your most problematic loan cannot be wiped.

Don’t wait too long to consider bankruptcy

Sometimes we believe that, if we are able, we have a moral duty to pay what we owe.

You should pay your bills if you are able to. Look into your possibilities for debt relief if you are having trouble. However, if your consumer debt (including the above-mentioned types that can be erased) exceeds half of your income or if it would take you five years or longer to pay it off, bankruptcy might be your best bet.

What you should know is as follows:

You require a bankruptcy lawyer: In the complex paperwork, it is easy to make a mistake that could lead to the dismissal of your case. In that case, you receive no relief, but the bankruptcy filing still lowers your credit scores.

Generally speaking, lawyers want to be paid up front: Although pro bono and legal aid services are available, they are frequently overburdened by demand. To find out what options are available if you are in dire need, give your local bankruptcy court a call. You might be able to find lawyers who are ready to take on some pro bono cases through your local bar association. If not, you will have to find some money to pay for filing for bankruptcy.

Do not wait too long: It is a common misperception that people declare bankruptcy when they have alternative options or at random. For the majority, the situation is very different. Some people spend money that may have been shielded from creditors in bankruptcy, including their retirement savings.